Since the Hong Kong SAR Government officially gazetted the legislation implementing the OECD’s Pillar Two model rules and the Hong Kong Minimum Top-up Tax (HKMTT), the tax compliance landscape for multinational enterprise (MNE) groups in Hong Kong has fundamentally shifted.

Under the latest regulations, any MNE group with annual consolidated revenues of €750 million or more is subject to a 15% global minimum tax rate on profits derived during fiscal years beginning on or after January 1, 2025. Following the official launch of the Inland Revenue Department’s “Pillar Two Portal” the first batch of qualifying enterprises has already begun submitting their initial top-up tax notifications. As we head into the 2027/28 year of assessment, the entire mechanism enters a critical phase of full operation and the first settlement of Top-up Tax Returns!

However, in assisting local Hong Kong enterprises with system integration, we have discovered a massive hidden risk: many MNE groups operating in Hong Kong that rely on Mainland China accounting systems (such as Kingdee, Yonyou, or Inspur) utilize legacy infrastructures completely unequipped to handle the highly sophisticated data extraction mandated by HKMTT!

Today, we will deep dive into a comprehensive analysis: under the new BEPS 2.0 regulations, what specific “localization gaps” cause Mainland ERP systems to suffer, and how can enterprises save themselves?

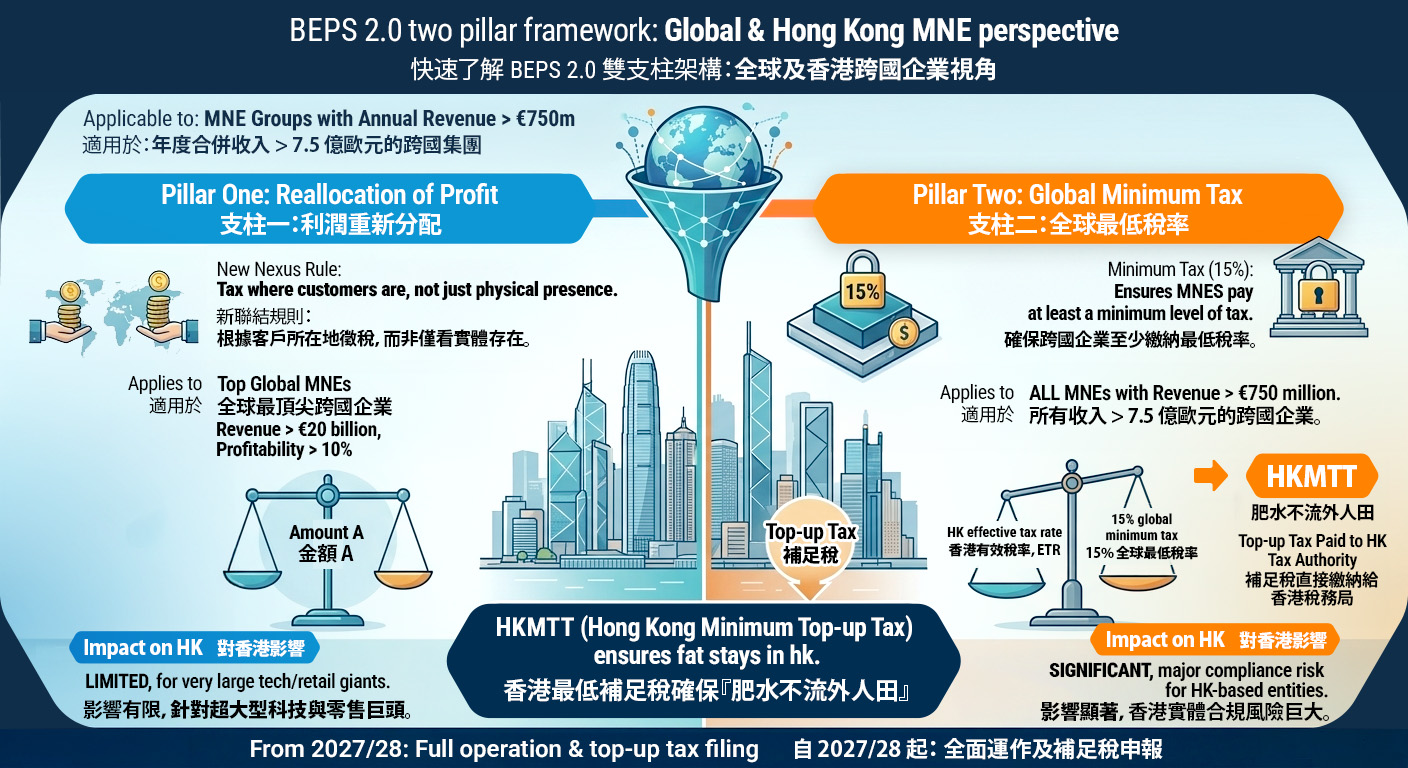

What are Hong Kong Minimum Top-up Tax (HKMTT) and BEPS 2.0?

Before breaking down the system mechanics, let’s look at a diagram to quickly understand the overall framework of this historic shift—the biggest overhaul in international tax law in three decades:

Simply put, BEPS 2.0 Pillar Two sets a global tax floor to end “race-to-the-bottom” tax competition among jurisdictions. Previously, many enterprises leveraged Hong Kong’s “territorial source principle” (Foreign-Sourced Income Exemption) to secure tax exemptions or exceptionally low effective tax rates on offshore income. Under the new rules, if an MNE group’s Effective Tax Rate (ETR) in Hong Kong falls below 15%, it must make up the difference via a top-up tax.

To implement the concept of “keeping tax revenues within local borders” the Hong Kong Government introduced HKMTT (Hong Kong Minimum Top-up Tax). Since the 15% differential must be paid regardless, it is better collected directly by the Hong Kong Inland Revenue Department.

Red Alert: 4 Compliance Pitfalls of Mainland Accounting Systems Under HKMTT

Many Mainland parent companies assume: “Our ERP handles China’s rigorous ‘Golden Tax Phase IV’ and fully digitalized e-invoices effortlessly; managing a straightforward 15% minimum tax rate in Hong Kong should be simple.”

This is a dangerous misconception. Mainland ERP tax modules are meticulously tailored around domestic Chinese tax regimes (such as Value-Added Tax and Corporate Income Tax). However, the “GloBE Income” used to calculate HKMTT is vastly different from standard accounting profits, demanding highly granular tax base adjustments. The following are 4 common bottlenecks faced by Mainland systems:

- GAAP Conversion and Parallel Accounting Pressures

- The Reality: Mainland accounting systems default to Accounting Standards for Business Enterprises (ASBE) and utilize RMB as their core functional currency.

- The Impact: HKMTT requires GloBE Income calculations to be built upon the accounting standard used in the ultimate parent entity’s consolidated financial statements (typically IFRS or US GAAP) or approved local standards like HKFRS. If your system cannot handle true multi-GAAP, multi-currency parallel accounting at its database layer, your Hong Kong subsidiaries face massive, error-prone manual ledger adjustments offline.

- Deficit in Data GranularityHKMTT calculations do not merely look at top-line figures; they require the extraction of hundreds of hyper-granular data points. For example:

- Substance-Based Income Exclusion (SBIE): Systems must isolate the exact value of Eligible Payroll for local employees and Eligible Tangible Assets physically located in Hong Kong to calculate tax carve-outs.

- Deferred Tax Recasting: Systems must support re-evaluating and tracking all historical deferred tax assets and liabilities at the specific 15% statutory minimum tax rate. Without pre-configured Substance Tags or custom fields in traditional Mainland systems, financial teams cannot generate OECD-compliant reports automatically.

- Lack of Automated Transitional Safe HarboursTo alleviate administrative burdens, the OECD provided the Transitional CbCR Safe Harbour framework. If an enterprise passes either the “De Minimis Test,” the “Simplified ETR Test,” or the “Routine Profits Test” for a jurisdiction, its top-up tax for that period is deemed zero.

- The Impact: Mainland systems lack built-in computational engines for Hong Kong or global BEPS 2.0 safe harbours, depriving companies of real-time monitoring and compliance alerts.

- Cross-Border Data Silos and Electronic GIR DisconnectStarting from the 2025/26 year of assessment, in-scope corporations in Hong Kong are mandatorily required to file profits tax returns electronically. Simultaneously, tax jurisdictions worldwide will begin exchanging the standardized GloBE Information Return (GIR). If your Mainland system operates on an isolated, domestic network or lacks open APIs to sync with international tax compliance software (e.g., Vertex, Thomson Reuters ONESOURCE), a critical data rupture occurs when transmitting information to global headquarters.

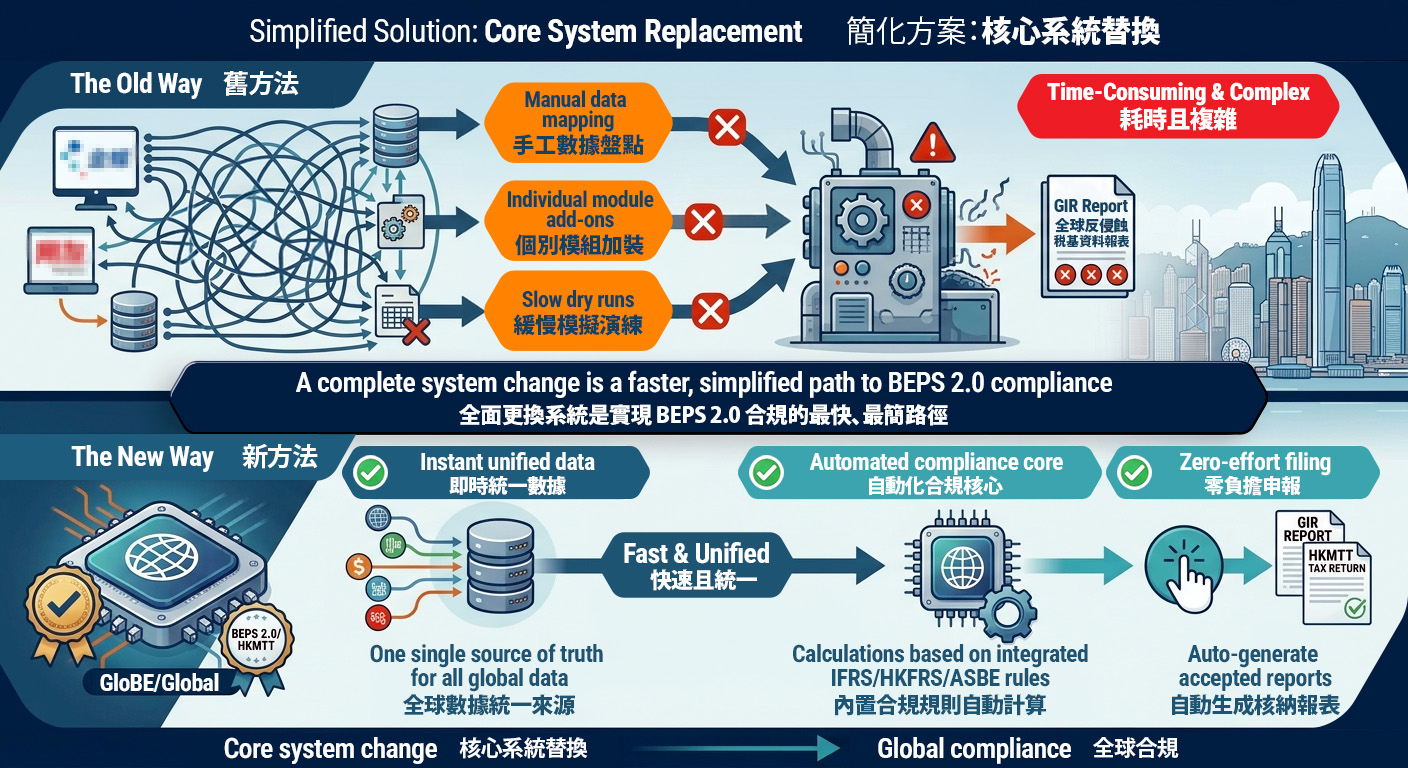

2027/28 Full Enforcement: Patching an Old System vs. a Core System Replacement

Because fiscal data for 2025 and 2026 has already accumulated within legacy setups, MNE groups relying on Mainland systems must make a strategic choice ahead of the 2027/28 filing season.

Historically, companies gravitated toward patchworks of “optimizations and modifications” on existing setups, but this route proves incredibly complex and labor-intensive in practice.

【The Old Way: Time-Consuming & Complex】

Manual Data Mapping ──> Individual Module Add-ons ──> Slow Dry Runs ──> High GIR Filing Risk ❌

❌ The 3 Hidden Compliance Landmines of “The Old Way”:

- Manual Data Mapping: Manually auditing accounts to identify data gaps for BEPS 2.0 (like specific payroll or tangible asset breakdowns) is highly prone to human error.

- Individual Module Add-ons: Forcing foreign Pillar Two modules onto an ERP architecture natively engineered for Mainland tax structures (like standard Kingdee/Yonyou deployments) creates massive integration friction and unstable system logic.

- Slow Dry Runs: When data remains siloed across isolated spreadsheets, every simulation requires laborious exports and imports, preventing timely validation of Transitional Safe Harbour eligibility.

✅ The Simplified Solution: Core System Replacement is the Fastest Path to Compliance

As visualized below, rather than perpetually patching incompatible legacy systems, a “Core System Replacement” provides the cleanest, fastest, and most straightforward path to full BEPS 2.0 compliance (The New Way):

The 3 Automation Advantages of “The New Way”:

- Instant Unified DataMigrating to a system natively engineered for global tax compliance creates an absolute One Single Source of Truth. It aligns HKFRS or IFRS data models smoothly in real time, eliminating manual data compilation.

- Automated Compliance CoreThe underlying engine has built-in global minimum tax (15%) and HKMTT calculation parameters. It automates multi-GAAP adjustments, multi-currency recalculations, and safe harbour checks behind the scenes.

- Zero-Effort FilingStop stressing over how to format data into OECD-compliant tables. The advanced system features “one-click generation” of IRD-compliant GloBE Information Returns (GIR) and domestic HKMTT returns, connecting directly to official electronic filing portals.

Expert Recommendation: Complete System Transition and Dry Runs

Do not wait until the 2027 official submission deadlines to discover that your system patches have failed. MNE groups should leverage the remainder of this year to transition to localized or globalized accounting platforms built with native BEPS 2.0 and HKMTT compliance capabilities. By retroactively processing your 2025 financial data through a modern, unified engine for comprehensive dry runs, you guarantee 100% automated, friction-free compliance when the 2027/28 filing window opens.

If your enterprise is experiencing compliance anxiety due to a mismatch between Mainland ERP architectures and Hong Kong’s new tax reality, contact our Professional Accounting System Consulting Team today. With deep expertise in cross-border ERP transitions and Hong Kong tax integration, we will construct a high-efficiency, risk-free transformation roadmap tailored to your business.